The restaurant food delivery business is changing rapidly as new online platforms compete to capture markets and customers in the Americas, Asia, Europe and the Middle East. Although these new Internet platforms are attracting considerable investment and high valuations (five already value at more than $1 billion), there is little real insight into market dynamics, growth potential, or customer behaviour. Based on a six-month study spanning 16 countries world wide McKinsey research, provides insight into this rapidly changing market.

Table of Contents

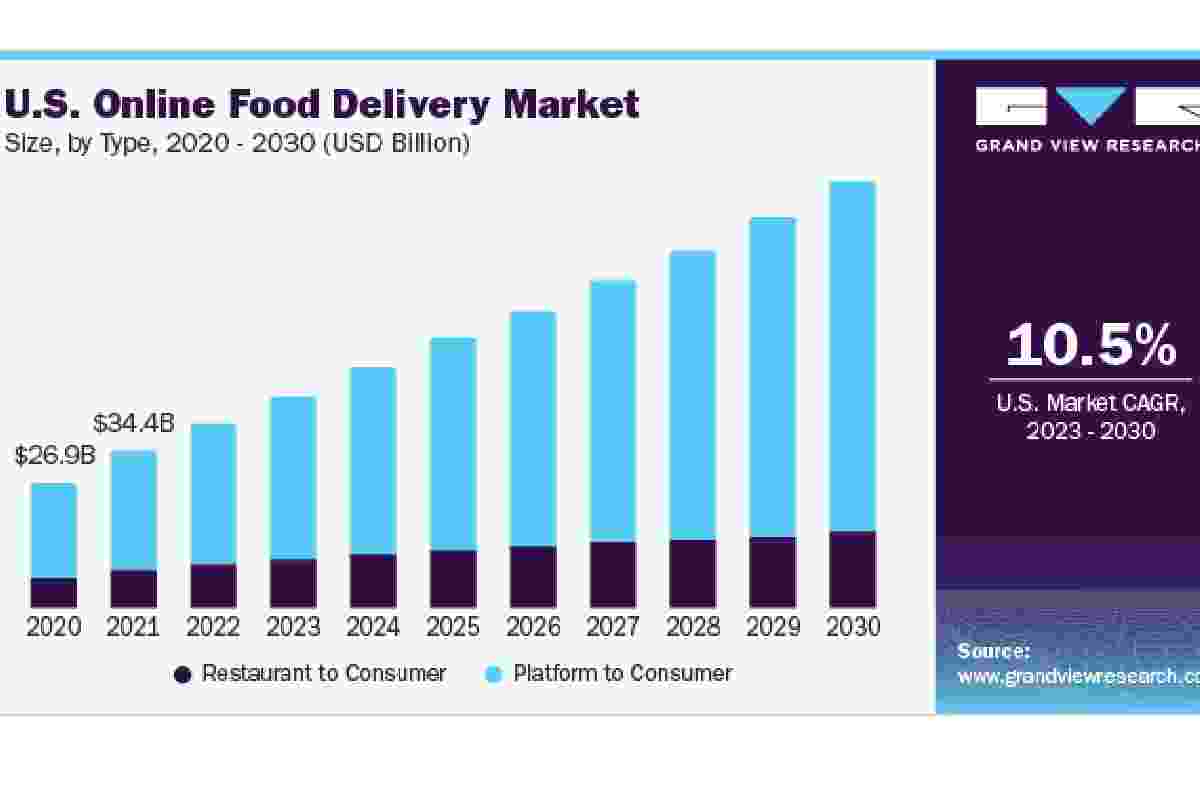

The Shape of the Market Today

Globally, the food delivery market is worth €83 billion, or 1% of the total food market and 4% of food sold in restaurants and fast food chains. It has matured in most countries, with an estimated global annual growth rate of just 3.5% for the next five years.

The most common form of delivery is the traditional model, in which the consumer places an order at the local pizzeria or Chinese restaurant (although many other types of restaurants, especially in urban areas, now offer delivery) and waits for it to arrive. The restaurant brings the food to the door. This traditional category has a 90% market share, and most of these orders, nearly three-quarters, are still placed over the phone.

However, as in so many other sectors, the rise of digital is reshaping the market. With maximum comfort and transparency, consumers accustomed to buying online through applications or websites increasingly expect the same experience when ordering dinner.

Two Tiers for Online Food Delivery

Two types of online platforms have emerged to fill this gap. The first type is the “aggregators”, which appeared about 15 years ago; the second is the “new delivery players,” which emerged in 2013. Both allow consumers to compare menus, scan and post reviews, and order from multiple restaurants with a single click. Aggregators, which fall into the traditional delivery category, take orders from customers and send them to restaurants, which do the delivery themselves. On the other hand, new delivery players are building their own logistics networks, providing delivery to restaurants that do not have their drivers.

Also Read: https://www.mombeautytips.com/the-indoor-flowering-plants/

Aggregators

Aggregators build on the traditional food delivery model, providing access to multiple restaurants through a single online portal. Consumers can quickly compare menus, prices, and peer reviews by logging into the site or app. Aggregators take a fixed margin on orders, which the restaurant pays, and the restaurant handles the actual delivery.

There is no additional cost to the consumer. With their asset-light model, aggregators post earnings before interest, taxes, depreciation and amortization (EBITDA) margins of 40-50%. Although investment continues to pour in (Delivery Hero and Foodpanda, for example, attracted €100 million in new investment in 2015), most of the consolidation in this subcategory has already occurred. Four players – Delivery Hero, Foodpanda, GrubHub and Just Eat – have reached a global scale.

These four players tend to focus on different regions. Nationally, two or three competitors typically dominate, driven primarily by their ability to build a large user base. Consolidation is well advanced in most markets and is likely to continue. McKinsey research shows that only 26% of standard delivery orders place online today, but we expect that proportion to overgrow.

New Delivery

Like aggregators, the new delivery players allow consumers to compare offers and order meals from a group of restaurants through a single website or app. Above all, the players in this category also ensure the logistics of the restaurant. It allows them to open up a new segment of the home catering market: high-end restaurants that traditionally didn’t deliver. The restaurant pays the new deliverers with a fixed margin of the order, as well as with a small.